Kingfisher Group Half year results for the six months ended 31 July 2024 (unaudited)

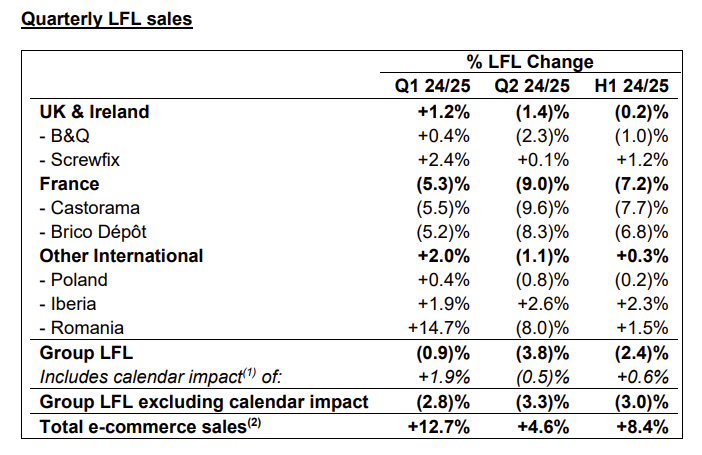

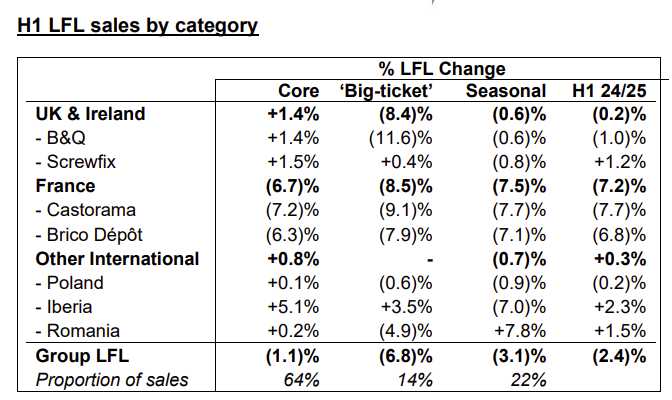

Finding growth in the European DIY Market has continued to be a challenge for Kingfisher with total sales down by -1.4% and LFL sales down by -2.4% YoY in the six months to 31st July. The UK fared better with total sales growing by 0.9% in the half year but LFLs were down by -0.2%. Screwfix was the stand-out performer with sales up by 4.5% and LFLs by 1.2%. B&Q sales were down by -1.2% and LFLs down by -1.0%. The "Core" business (representing 64% of turnover) grew across most of Europe (except France), whilst "Seasonal" and "Big Ticket" were largely in decline across most territories.Total sales -1.4% and LFL -2.4%. Q2 LFL -3.8%

- UK & Ireland (LFL -0.2%) and Poland (LFL -0.2%) both resilient despite weather-impacted seasonal sales; market share gains in all banners

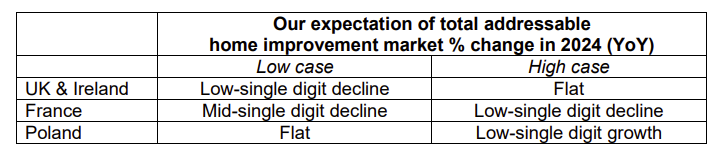

- France sales (LFL -7.2%) broadly in line with the market, reflecting the soft consumer backdrop throughout the period

- Resilient core category sales, supported by repairs, maintenance and existing home renovation activity. Recovery in seasonal sales since early July and weak ‘big-ticket’ sales as expected

- Strong results from e-commerce marketplace (Group GMV +80.0%). E-commerce sales penetration now 18.3% (H1 23/24: 16.8%)

- Good results in trade propositions (including TradePoint LFL +7.1%).

- Current trading: Q3 24/25 LFL sales (to date) -0.3%

Gross margin, costs and inventory

- Gross margin % +40bps with retail price inflation flat YoY

- Targeting c.£120m of cost reductions for the full year, weighted towards H1

- Net inventory, down £134m (4.3%) YoY

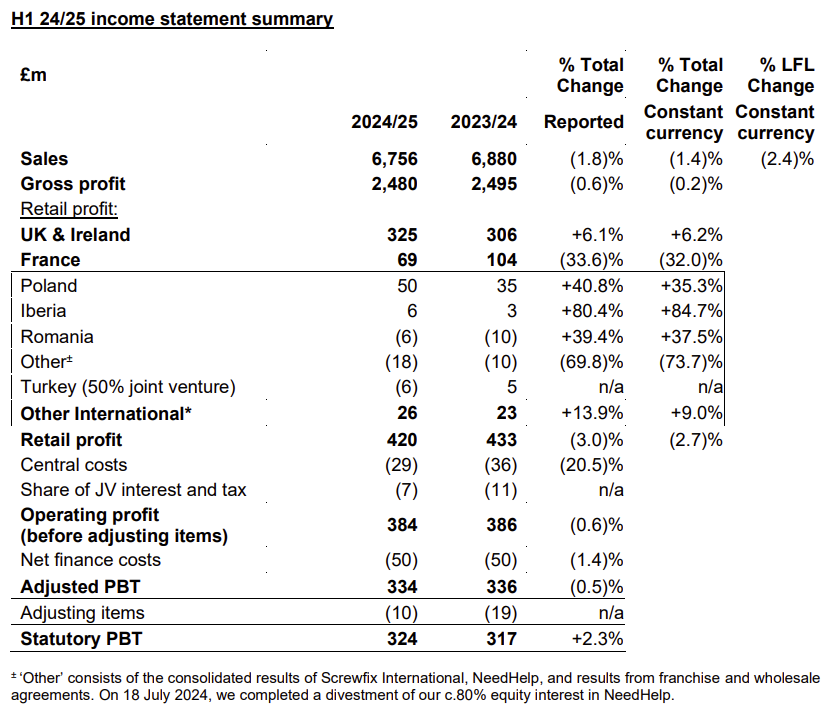

- Adjusted PBT down 0.5% to £334m, including c.£25m of one-off business rates refunds at B&Q.

- Statutory PBT up 2.3% to £324m

- Free cash flow of £421m, supported by phasing of inventory purchases over the year

Thierry Garnier, Chief Executive Officer, said: “Trading overall in the first half was in line with our expectations. This was underpinned by customers continuing to repair, maintain and renovate their existing homes, driving resilient volume trends in our core product categories. As expected, demand for ‘big-ticket’ categories has remained weak, in line with the broader market, while seasonal category sales trends have improved since early July. Against this backdrop we maintained a strong focus on effectively managing our costs and inventory.“Our UK & Ireland banners continued to gain market share, supported by strong e-commerce sales and our progress in addressing trade customer needs. Screwfix delivered positive LFL sales and TradePoint achieved strong LFL sales growth of 7.1%, now representing 22% of B&Q’s sales. Sales in France were broadly in line with the market, reflecting the soft consumer backdrop. Notwithstanding this, we are making rapid progress with our actions to simplify the French organisation and improve the performance and profitability of Castorama France over the medium term. In Poland, we gained market share and our sales trend was supported by an improved consumer environment.“I am proud of the unwavering focus of our teams in executing against our strategic priorities, with two key highlights. First, our e-commerce sales penetration improved by 1.5 points to 18.3% and B&Q’s e-commerce marketplace reached a 40% share of its online sales. We have also successfully launched Castorama France’s marketplace, with Poland to follow in H2. And second, in trade, we are extending the successes we have seen in the UK to other markets, with trade sales penetration growing strongly in France, Iberia and Poland.“Reflecting our performance in the first half and our current view of the trading environments in our markets, we have tightened our profit guidance and upgraded our free cash flow guidance for the year. We remain focused on continuing to manage our costs and cash effectively, and driving further market share gains by delivering on our key strategic priorities.“With positive early signs of a housing market recovery, notably in the UK, Kingfisher is strongly positioned for growth in 2025 and beyond.”

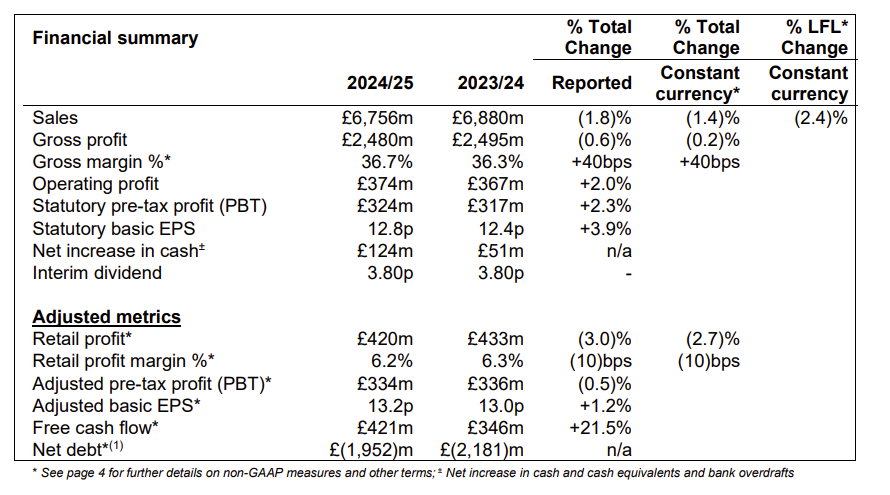

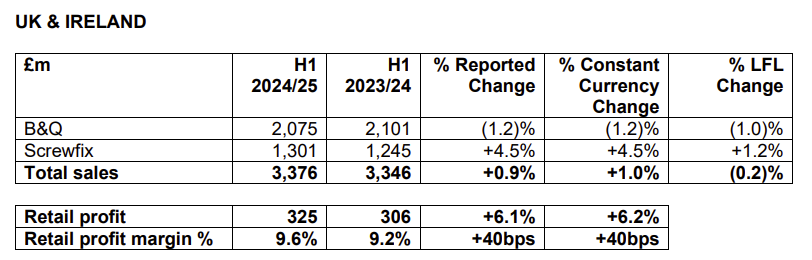

H1 24/25 results• Total sales -1.4% (constant currency) and -1.8% (reported)• LFL sales -2.4% including a +0.6% leap year impact− Q2 LFL sales -3.8%, including a -0.5% calendar impact− Q1 LFL sales -0.9%, including +0.8% calendar impact and +1.1% leap year impact• Sales by region:− UK & Ireland* LFL -0.2%: market share gains at B&Q supported by strong e-commerce and TradePoint sales; market share gains and positive LFL at Screwfix− France* LFL -7.2%: reflecting the broader market. Castorama and Brico Dépôt performed broadly in line with market− Poland LFL -0.2%: sales trend supported by improved consumer environment and trade customer initiatives; performance ahead of the market

• Sales by category:− Core* (64% of sales): continued resilience (LFL -1.1%) driven by repair, maintenance and renovation activity on existing homes− ‘Big-ticket’* (14% of sales): weak sales as expected (LFL -6.8%) reflecting trends across the broader market− Seasonal* (22% of sales): lower sales (LFL -3.1%) given unfavourable weather conditions across much of April to June

• Retail price inflation flat year-on-year (YoY); negative mix impact on average selling price from lower ‘big-ticket’ sales. Overall volume lower YoY, with stable underlying volume trends in core categories between Q1 and Q2• Total e-commerce sales* +8.4%, driven by growth in the UK & Ireland− E-commerce sales penetration* of 18.3% (H1 23/24: 16.8%)− Continued strong growth of e-commerce marketplace sales at B&Q and Brico Dépôt Iberia*; Group marketplace GMV* +80.0% YoY• Gross margin % +40 basis points to 36.7% (H1 23/24: 36.3%) reflecting effective management of product costs, retail prices and supplier negotiations, and lower clearance costs and stock provisions• Retail profit -2.7% in constant currency to £420m (H1 23/24: £433m), reflecting lower profits in France and higher losses from our joint venture in Turkey; partially offset by higher profits in the UK & Ireland and Poland• Statutory PBT +2.3% to £324m (H1 23/24: £317m), reflecting higher operating profit (including lower adjusting items* YoY)• Adjusted PBT -0.5% to £334m (H1 23/24: £336m), reflecting lower retail profit, largely offset by lower central costs* and share of JV interest and tax• Free cash flow of £421m, up £75m (H1 23/24: £346m), reflecting working capital inflow and lower capital expenditure• Net increase in cash of £124m (H1 23/24: £51m), reflecting higher free cash flow• Net debt down to £1,952m (31 January 2024: £2,116m), including £2,324m of lease liabilities under IFRS 16 (31 January 2024: £2,367m), reflecting the net increase in cash. Net debt to last twelve months’ EBITDA* of 1.5x (31 January 2024: 1.6x)• Interim dividend per share declared of 3.80p (FY 23/24 interim dividend: 3.80p)

.png)