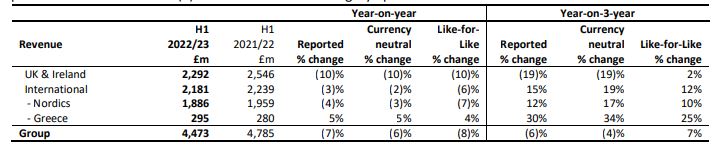

For the six-month period ending October 29, 2022, Currys reported an loss before tax of £17m, down £62m year on year. International profit before tax was down 94%Group like-for-like sales were down 8% to £4.4bn. UK and Ireland sales decresed 10% to £2.2bn, while international sales slipped 6% to £2.1bn.

Unaudited Results for the Half Year Ended 29 October 2022 - released 15th DecemberKey Highlights• UK&I profit growth as gross margin improvements and cost savings offset sales decline• International profits down significantly due to actions taken in face of competitors’ heavy discounting• Cost savings: UK&I programme well on track for £300m saving target, International offsetting inflationary pressures• Online share of business stable, highlighting strength of omnichannel model following pandemic disruption• UK&I Credit adoption of 17%, +460bps YoY and well ahead of 16% target for 2023/24Financial Performance• Group LFL (8)% (Yo3Y +7%); Revenue (7)% (Yo3Y (6)%)• Group adjusted loss before tax £(17)m, down £(62)m YoY due to lower International profits• Group statutory loss before tax £(548)m driven by non-cash goodwill impairment of £(511)m• Period-end net debt £(105)m with significant liquidity headroom given total revolving credit facilities of £676m• Pension deficit decreased slightly to £(251)m (30 April 2022: £(257)m, 30 Oct 2021: £(416)m) despite market volatility• Interim dividend of 1.00p declared (flat YoY).Current Year Guidance: "Reflecting the strength of the UK&I business and the disruption to our International markets, we now expect full year PBT to be between £100-125m, with cash generation in the second half".Alex Baldock, Group Chief Executive“Currys UK&I performance continues to strengthen, and is showing real momentum, reflecting good progress in our transformation. International, however, has had a tough period, and faces short-term but intense pressures from adisrupted market.. In the UK&I, our profits are up, from increased gross margins and strong cost discipline. We’re bucking the trend with world-class and increased colleague engagement. Our customers are happier too, and are more likely than ever torecommend us. We are making more of our winning Omnichannel model and are building more Customers for Life with strong Services growth. Our International business, which has consistently delivered growth in sales and profits over many years, has had adifficult first half with margins sharply down. Lower demand has left domestic competitors with excess stock, which they’re now heavily discounting. This has substantially disrupted the market, and required margin investment to keepour sales strong. We expect these pressures, intense though they are, to be temporary - demand will normalise, excess stock will wash through, and competitors will find unprofitable aggression hard to sustain. We’ve also steppedup our self-help actions on margins and cost. Of course, our customers are feeling real cost of living pressure and our job is to help them get hold of the technology that’s more essential to their lives than ever. We’re doing that, through our price promise, giving customers access toresponsible credit, and offering more products that save them money through lower energy costs. Our Go Greener range is flying off the shelves. It’s a tough environment, and we are planning for that to continue. Still, we expect to maintain the trajectory ofimproving UK&I profitability and a robust recovery in International profits. Our ever-improving customer experience and strong Services give us confidence in improving margins. And we will continue our excellent progress on costefficiency. We have a strong balance sheet and a strategy that’s working. By focusing on the things we can control, while doing everything we can to support our colleagues and customers, we’ll ride out the current turbulence and emerge aneven stronger business well-set for long-term success.”UKTotal UK&I sales declined (10)%, driven by like-for-like sales decline of (10)%.Compared to pre-pandemic levels, UK&I like-for-like sales are up +2%.During the period, the online share of business was 43%, flat YoY. Compared to three years ago online share of business is up +17ppts as customers have benefited from the improvement to our online-only propositions as themarket has shifted towards online.Domestic appliances and Mobile were the strongest performing categories due to our investment in these areas and improved availability. Consumer Electronics and Computing both saw sales decline, albeit the strong growth inComputing over the pandemic meant sales were still healthily up on three years ago.The UK market shrank (7)% during H1 with the online market reducing by (10)% and the store channel declining less than (2)%. Compared to three years ago, the market is +14% larger as the online market growth of +62% hascompensated for a (23)% decline in the store channel. Our market share is down (120)bps compared to last year as we lost share in consumer electronics and computing. Our market share is down (200)bps on three years ago due tothe shift away from stores where we historically had higher share. In stores, our share is stable, and we have gained share online.In UK&I adjusted EBIT increased +25% YoY and was higher than three years ago. Improvements to gross margin were driven through higher customer adoption rate of credit and other services (especially online), improved use of dataand analytics to drive better returns on marketing and promotions, cost savings and the introduction of two-person delivery charges towards the end of the period. Operating costs fell in absolute terms as savings offset inflationarycost pressures and increased business rates tax.We have recorded a £(511)m non-cash impairment of UK&I goodwill that arose at time of Dixons Carphone merger in 2014. This was primarily driven by increased discount rates as a result of the sharp increases in UK gilt yieldsaround our period end, as well as more prudent economic assumptions within our internal valuation models.Gross margins increased +160bps, as the investment in long-term transformation activities has yielded improvements in bundling, upselling and adoption rate of credit and other services. The operating expense to salesratio worsened by (130)bps as costs reduced in absolute terms, but not enough to offset the decline in sales. A £(14)m headwind from the lowering of UK & Ireland business rates tax reliefs, energy cost inflation of £(11)m andwage inflation of £(4)m were more than offset by cost savings across supply chain, store operations and central costs as well as lower depreciation.InternationalIn International, adjusted EBIT declined (94)% YoY and is also down significantly on three years ago. This was driven by gross margin erosion as some smaller domestic competitors are following aggressive growth strategies to gainshare in a market that is structurally bigger following the pandemic. They substantially overestimated demand and the excess stock bought into market is being cleared at discounted prices. Against this backdrop, we deliberatelykept pricing competitive to preserve market share in what we expect to be a temporary period of depressed market profitability. Demand will normalise, the excess stock will sell through, and the smaller competitors are unlikely to beable to sustain these unprofitable practices.Due to lower International profitability, operating cash flow declined (54)% YoY, while free cash flow was an outflow of £(86)m reflecting the lower operating profitability , normalized levels of investment and a small, expected workingcapital outflow.View Currys results