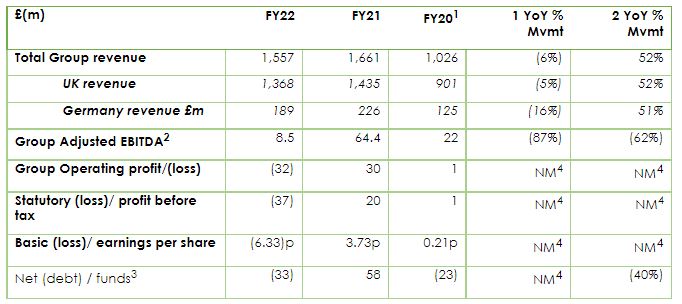

In FY22 (the 12 months ending 31 March 2022), AO Group sales declined by 5% on FY21 in the UK and by 6% across Europe. The group grew extraordinary quickly in FY21 and FY22 sales are 52% ahead of FY20.The profit performance was challenging with a statutory loss before tax of £37m (FY21: profit of £20m).£40m of capital was raised in recent months and a £80m revolving credit facility was extended until April 2024.Financial highlights

- Group revenue growth of 52% over two-year period since FY20; resilient performance in our UK business with a one YoY decline of 5% against an extraordinary comparative performance during Covid in FY21

- Group EBITDA of £8.5m impacted by increased staff costs added during Covid in H2 FY21as well as increased marketing and logistics costs

- Statutory loss before tax of £37m (FY21: profit of £20m)

- Overall liquidity of £50m (FY21: £143m) at 31 March 2022 with net debt of £33m (31 March 2021: £58m net funds)

- Capital-raising post year-end successfully secured additional liquidity of £40m with £80m revolving credit facility extended until April 2024

Operational highlights

- Over four million new customers experienced AO's customer service (FY20-FY22), with repeat purchase rates continuing to outperform pre-Covid levels

- Over 350,000 Trustpilot ratings, averaging an "Excellent" 4.6/5 stars and Net Promoter Scores

- New agreement with Homebase to supply appliances and installation and recycling services to Homebase's customers where Homebase agrees to purchase exclusively from AO their MDA and audio-visual appliances over an initial five-year term

- AO decided to close German business post year end with estimated closure cash costs to be no more than £5m.

- Over five million appliances, including two million fridges, have now been recycled at the AO Recycling facility.

- "AO has a share in MDA of 18% and an 32% overall online market share".

Outlook

- Trading through the first quarter of FY23 has remained broadly in-line with the Board's expectations for FY23, with revenues in the approximate range of £1bn to £1.25bn

- Group adjusted EBITDA for FY23 forecast to be in the range of £20m - £30m.